CySEC amends criteria for determining significant Cyprus investment firms

The Cyprus Securities and Exchange Commission (CySEC) has redefined the threshold criteria that determines a ‘significant CIF’ for the purposes of the Investment Services and Activities and Regulated Markets Law of 2017, as amended, in light of a new prudential framework for investment firms (IFR/IFD).

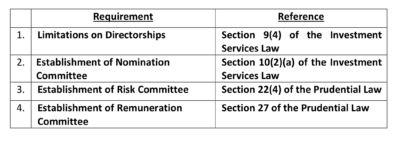

As per section 9(4) of the Investment Services Law, unless representing the Republic, members of the board of directors of a CIF that is significant in terms of its size, internal organization and the nature, scope and complexity of its activities, shall not hold more than one of the following combinations of directorships at the same time:

- (a) one executive directorship with two non-executive directorships;

- (b) four non-executive directorships

As per section 10(2)(a) of the Investment Services Law, a CIF which is significant in terms of its size, internal organization and the nature, scope and complexity of its activities, shall establish a nomination committee composed of members of the board of directors that do not perform any executive function in the CIF.

Section 26(8)(a) of the Prudential Law refers to a CIF where the value of its on and off‐balance sheet assets is on average equal to or less than EUR 100 million over the four‐year period immediately preceding the given financial year.

Thus, if a CIF’s on and off-balance sheet assets are on average greater than EUR 100 million over the four-year period immediately preceding the given financial year, it should establish a remuneration committee and a risk committee according to the provisions of the Prudential Law mentioned above.

For consistency purposes over governance requirements between the Investment Services Law and the Prudential Law, a CIF shall be considered as a ‘significant CIF’ for the purposes of the Investment Services Law where its on and off-balance sheet assets are on average greater than EUR 100 million over the four‐year period immediately preceding the given financial year.

CIFs should, within four months from the end of each of their financial year, assess whether they meet the threshold defined in point 6 above to become a ‘significant CIF’ for the purposes of the Investment Services Law and for the purposes of sections 22(4) and 27 of the Prudential Law.

If a CIF meets the threshold criteria, then it should:

- (a) take all necessary measures to comply with the requirements that apply to a ‘significant CIF’ as per the Investment Services Law,

- (b) take all necessary measures to comply with the relevant requirements of the Prudential Law and

- (c) forthwith inform CySEC accordingly and submit its new organisational structure through CySEC’s portal.

This assessment is considered as valid until the next assessment is made for the following year. CySEC notes that annual assessments should always take into consideration the four-year period immediately preceding the given financial year.

Where a CIF has been in business for less than four years, for the purposes of the above assessment it shall use its on and off-balance sheet assets for the periods available.

Therefore, a CIF that after the above assessment has on and off-balance sheet assets1 on average greater than EUR 100 million over the four-year period immediately preceding the given financial year, it must make arrangements to establish and have in place sound, effective and comprehensive strategies, processes and systems to achieve compliance with the following requirements: