ASX sees net profit decline in FY24

ASX today posted its financial results for the fiscal year to June 30, 2024.

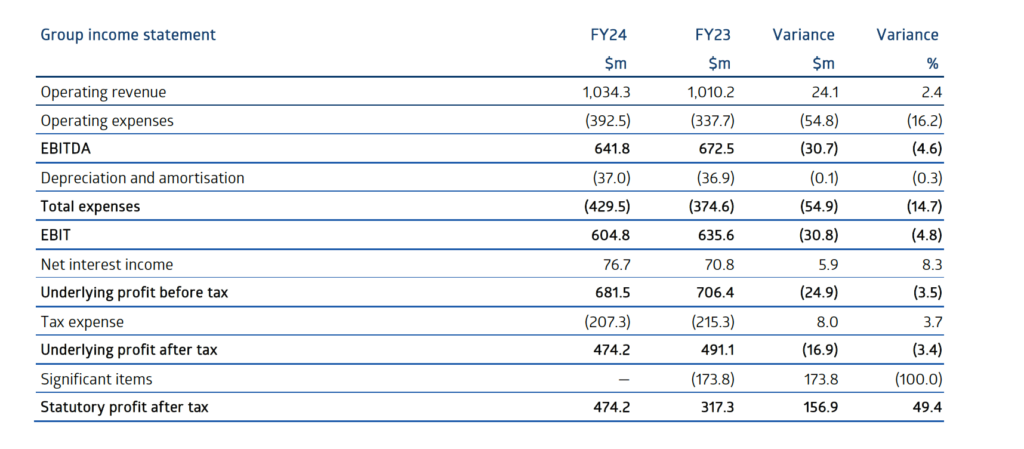

ASX delivered FY24 operating revenue of $1.03 billion, a 2.4% increase on the prior corresponding period (pcp) and a record revenue performance for ASX.

Performance across ASX’s four lines of business was mixed, with growth in Markets and Technology & Data offset by lower contributions from Listings and Securities & Payments. Markets revenue was $315.4 million, up 7.9%, reflecting higher futures volumes with significant growth in the traded volumes of 90 day bank bill futures, and 3 year and 10 year treasury bond futures in particular. Technology & Data revenue was up 5.9% to $255.1 million, driven by an increase in equities and futures market data distribution, and growth in customer connections at the Australian Liquidity Centre (ALC).

Lower activity in cash equities clearing and settlement services impacted the Securities & Payments division, with revenue down 1.1% to $255.6 million. Cyclically low levels of capital markets activity also impacted the Listings business, reflected in total revenue for the division down 4.8% to $208.2 million.

Total expenses for the Group increased 14.7% to $429.5 million, reflecting an increase in employee costs to support investment for regulatory commitments and technology initiatives, as well as higher equipment and administration costs, and ASIC supervision levy. The total expense growth rate for FY24 was in line with previously stated guidance of ~15%.

Underlying net profit after tax (NPAT) was down 3.4% at $474.2 million. This decline was driven by higher operating expenses, and was partially offset by operating revenue growth and increase in net interest income. Net interest income increased 8.3% on the pcp primarily driven by higher returns on ASX cash balances exposed to the rising interest rates.

A fully franked final dividend of 106.8 cents per share (cps) will be payable on 20 September 2024. The total dividend per share for FY24 of 208.0 cents is 8.9% lower than the prior year, reflecting the decrease in underlying NPAT and a lower dividend payout ratio of 85% in FY24 (90% in FY23).

In terms of guidance, FY25 total expense growth is expected to be within the previously stated range of between 6% and 9%2. FY25 capital expenditure guidance of $160 million to $180 million will primarily support the indicative technology modernisation roadmap.