Plus500 registers 18% Y/Y rise in revenues in Q1 2026

Online broker Plus500 Ltd (LON:PLUS) today provided a trading update for the three-month period ended 31 March 2026.

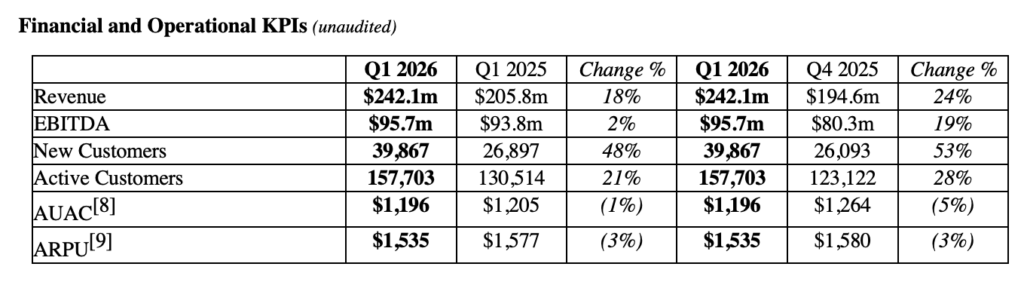

Revenue and Customer Income both increased strongly in Q1 2026, with revenue rising by 24% from the fourth quarter to $242.1m (Q1 2025: $205.8m; Q4 2025: $194.6m), including trading income of $231.7m and interest income of $10.4m. The revenue rise in annual terms was 18%.

Customer Income increased by 33% quarter on quarter to a five-year record high of $270.6m (Q1 2025: $176.3m; Q4 2025: $202.7m), reflecting strong customer engagement and trading activity during the period.

Customer Trading Performance was ($38.9m) in Q1 2026 (Q1 2025: $15.4m; Q4 2025: ($20.2m)), and is expected to remain broadly neutral over time.

New Customers increased by 53% quarter on quarter to 39,867 (Q1 2025: 26,897; Q4 2025: 26,093), as the Group continued to scale its global customer base while maintaining a strategic focus on attracting higher value customers.

Average user acquisition costs (AUAC) decreased by 5% quarter on quarter to $1,196, demonstrating the strength and flexibility of the Group’s marketing efficiency and disciplined capital allocation. Higher customer volumes were achieved alongside a reduction in acquisition costs, while customer value continued to increase over time. This was achieved alongside an additional investment in customer acquisition of approximately $16m during the quarter, above the prior year quarterly run-rate, with improving cohort quality further supporting long-term revenue.

EBITDA increased by 19% quarter on quarter to $95.7m (Q1 2025: $93.8m; Q4 2025: $80.3m), equating to an EBITDA margin of 40%, reflecting the flexibility of the Group’s operating cost base and its ability to invest in growth while maintaining strong profitability. On a constant currency basis, underlying performance was even stronger, with reported results impacted by FX-related cost headwinds during the period.

Customer engagement remained strong, with Active Customers increasing by 28% from the preceding quarter to 157,703 (Q1 2025: 130,514; Q4 2025: 123,122), reflecting higher levels of trading activity across the Group’s platforms.

Average revenue per user (ARPU) was $1,535 during the quarter (Q1 2025: $1,577; Q4 2025: $1,580). The Group expects to generate increasing value from these cohorts over time, in-line with previous trends, as the current ARPU reflects a higher weighting of new customers.

Total customer deposits reached a record quarterly level of $1.8bn (Q1 2025: $1.6bn; Q4 2025: $1.7bn), reflecting strong customer demand and the quality of newly acquired customers. High deposit volumes during the quarter led to approximately $4m in additional payment processing costs.

The Group remained debt-free and maintained a strong financial position, with cash balances of over $780m as of 31 March 2026 (31 December 2025: $801.6m).

The Group entered FY 2026 with strong momentum, driven by continued growth in customer acquisition, increasing customer value and expansion across both its OTC and non-OTC businesses.

The Group’s growing presence in the US futures and prediction markets, combined with the increasing value and quality of its customer cohorts, is expanding its addressable market and strengthening the sustainability of its earnings profile. Reflecting this strong performance and outlook, the Board expects FY 2026 revenue and EBITDA to be ahead of current market expectations.

The Group delivered strong momentum in its US business, with revenue of approximately $35m in Q1 2026, representing an increase of c.21% QoQ and c.45% YoY, driven by growth across both its B2B and B2C offerings. The continued growth of the US business reinforces its position as a key pillar of the Group’s diversified earnings base in a core strategic growth market.

In February 2026, the Group successfully launched its US B2C prediction markets offering, enabling retail customers to access regulated event-based contracts through an enhanced user experience and broader product suite.

The Group also continued to expand its B2B prediction markets offering, building on its strategic partnerships, including its landmark appointment as clearing partner for the CME Group and FanDuel’s event-based contracts platform.

The Mehta acquisition marks a major milestone in the Group’s global futures strategy, providing immediate access to India, one of the world’s largest retail derivatives markets, and creating opportunities for further scale through targeted synergies with its existing operations in the US futures market.

The Indian market provides attractive long-term structural growth fundamentals, including high retail participation and deep derivatives liquidity, presenting a compelling opportunity for Plus500.

The Group’s OTC business delivered a strong performance during the quarter, supported by increased customer engagement and trading activity across its platforms. Leveraging its global customer base of c.34 million registered customers, the Group continued to enhance the value of its customers through its data-driven acquisition capabilities, enabling efficient acquisition at attractive AUAC levels. Increasing customer value has been accompanied by lower acquisition costs, reflecting the strength and scalability of the Group’s operating model, as well as its unique technological capabilities, which provide a distinct competitive advantage.

Continued improvements in customer retention, monetisation and activation are driving increased engagement and value across the Group’s higher quality customer base. The average deposit per Active Customer remained robust, with further expansion driven by increased deposits from OTC customers, reflecting the Group’s continued success in acquiring higher value customers.