Cboe Silexx adds new Box Spread option to strategies, enhances Copy Quote feature in Multi Order Ticket

Cboe has unveiled a set of enhancements to Cboe Silexx, a multi-asset order execution management system (OEMS) that caters to the professional marketplace.

Version 26.8 of Cboe Silexx has a new Box Spread option added to the Add Strategy menu, as well as enhances the Copy Quote feature in the Multi Order Ticket.

- Box Spread Strategy Support | Multi Order Ticket

A new Box Spread option has been added to the Add Strategy menu. When selected, it constructs a four-leg box spread using a single strike width based on the existing leg. The system determines whether the user is building a long (lend) or short (borrow) box based on the side of the initial leg. Legs are ordered as: low-strike Call, low-strike Put, high-strike Call, high-strike Put.

![]()

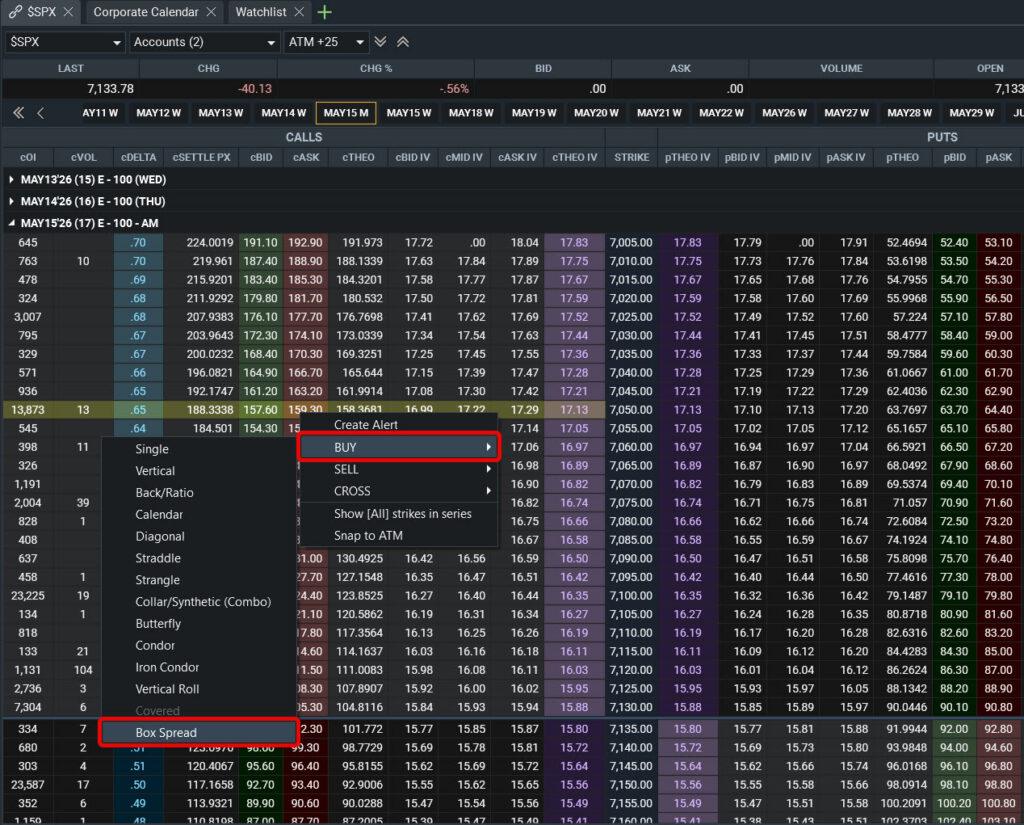

- Box Spread Strategy Support | Option Chain

Users can now buy or sell a box spread directly from the Option Chain right-click context menu. The selected strike is treated as the low strike, and the system automatically constructs the remaining three legs with a single strike width offset, following the same ordering convention.

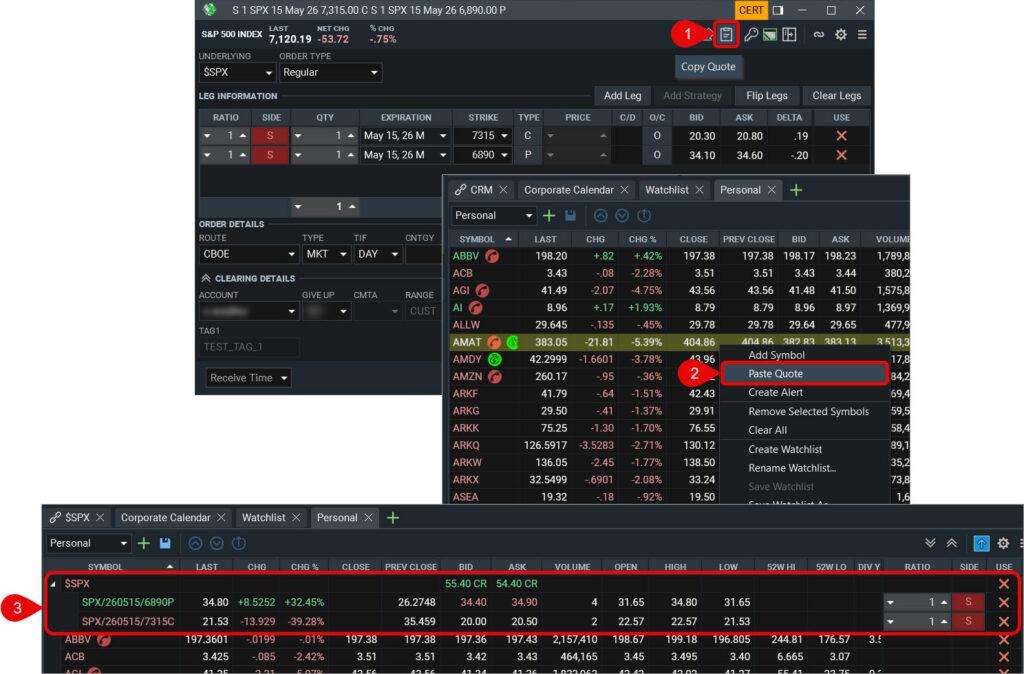

- Multi Order Ticket | Copy Quote to Watchlist Enhancement

The Copy Quote feature in the Multi Order Ticket has been enhanced to support pasting strategies directly into a Personal Watchlist. After building a strategy in the Multi Order Ticket, click the Copy Quote button, then right-click in a Personal Watchlist and select Paste Quote to add the strategy. The pasted strategy includes all leg details (expiration, strike, type), leg ratios, and leg sides. Once pasted, the clipboard is consumed and the Paste Quote menu item is disabled until a new quote is copied. This feature does not apply to FLEX instruments or the Quick Ticket.

- Portfolio | FLEX Position Values

FLEX option positions in the Portfolio module are now fully populated with live analytics powered by streaming theoretical values. Previously, many FLEX fields were blank. The following fields are now populated for FLEX positions:

- Pricing:Mark (utilizes Theo), Premium (extrinsic value), Theo, Market Value

- Greeks:Delta, Gamma, Theta, Vega, Rho, and their contract-level equivalents (Delta Contr, Theta Contr, Vega Contr)

- P&L:PnL Net, PnL Unrealized, PnL Trading, FX P&L

- Exposure:Gross Exposure, Long Exposure, Short Exposure, $ Delta

- Other:ITM/OTM status, First Trade Date, Earnings date, Ex-Dividend date

FLEX positions are also now included in grouped summaries and quantity roll-ups alongside standard options.