CMC Markets reports 50% Y/Y drop in leveraged trading revenue in H1 2022

Online broker CMC Markets Plc (LON:CMCX) today posted its interim results for the six months to September 30, 2021, with revenues sharply down from the year-ago period.

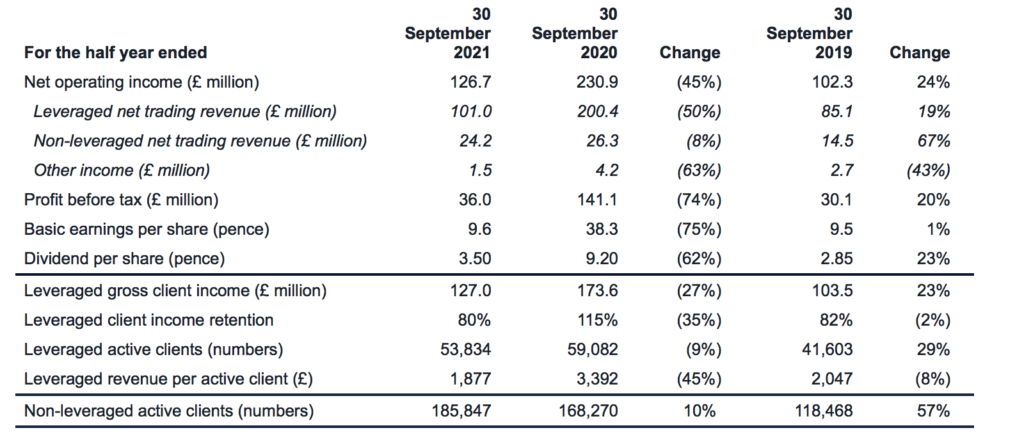

H1 2022 leveraged net trading revenue was £101.0 million (H1 2021: £200.4 million). The reduction is a result of a decrease in market volatility resulting in lower client trading activity throughout the period and lower client income retention.

Client income retention for the period stood at 80%, broadly in line with target and is expected to continue to recover through the rest of the year. H1 2022 leveraged active clients are 9% lower compared to H1 2021, but monthly trading client numbers continue to remain close to record highs and importantly are still up 29% versus pre-pandemic H1 2020 levels.

On the brighter side, total AUM in the leveraged business stood at £557 million, a new period-end record high. The Group’s strategic initiatives across the leveraged business remain unchanged.

The Group’s non-leveraged net trading revenue was £24.2 million for H1 2022 (H1 2021: £26.3 million). Underlying active client numbers are up 10% versus H1 2021, now standing at 185,847. Client non-leveraged Assets Under Administration (“AUA”) reached a new record high at AU$74.8bn, up 30% versus H1 2021 and up 67% versus pre-pandemic H1 2020 levels.

During September 2021 CMC announced the acquisition of Australia and New Zealand Banking Group Limited’s (“ANZ”) Share Investing client base for a sum of AUD$25 million. The transaction involves the acquisition of approximately 500,000 ANZ Share Investing clients, with total assets in excess of AUD$45 billion. The AUD$25 million consideration will be funded from the Group’s existing cash resources.

With this acquisition, the existing white label technology partnership, which has seen CMC’s trading technology power ANZ’s share investing business since 2018, will come to an end. The existing white label partnership generated £39.5 million in net trading revenue for CMC in FY 2021 and £16.7 million in H1 2022. The CMC platform will offer clients a wide range of additional benefits currently unavailable with ANZ. These include access to enhanced, market-leading mobile apps and complementary education tools and resources.

Following transition, the legacy ANZ Share Investing clients will benefit from lower brokerage charges across four major international markets and the local Australian market, and will give CMC the opportunity to drive greater value from its enlarged client base.

The transaction further establishes CMC as a financial technology leader in the Australian market and removes the uncertainty around the finite term of the existing ANZ white label partnership. The transaction is expected to take 12 to 18 months to fully transition clients and is another significant step in the ongoing diversification of the Group’s global business.

Regarding regulatory environment, CMC Markets notes that the Australian Securities and Investments Commission (ASIC) announced new regulatory measures relating to CFDs in October 2020 that came into effect on 29 March 2021.

“We are supportive of the regulatory change, as we have always operated to the highest standards, and our experience with the European Securities and Markets Authority (“ESMA”) measures show that they are, in the medium to long term, positive for CMC and our clients,” CMC Markets says.

These regulatory changes reduced the notional value of retail client trading in Australia, the broker says. This, combined with lower market volatility, resulted in less active client trading than in the prior period, in line with CMC’s expectations and with that seen in the ESMA region in FY 2019.

Regarding its institutional business, CMC Markets notes that, looking at the growth of its Australian non-leveraged business over the past decade, it has been built on B2B partnerships. The company now has some 160 B2B partners across the region. It sees a similar opportunity for it to utilise the same strategy in the UK non-leveraged business. On the leveraged side, CMC continues to pursue leveraged institutional and B2C opportunities and its institutional offering continues to provide great growth potential for both business lines.

The Group is maintaining its dividend policy at 50% of profit after tax. The Board has declared an interim dividend of 3.50 pence per share (2021: 9.20 pence per share), with a view to paying a final dividend in line with the Group’s policy. The interim dividend will be paid on 20 December 2021 to those members on the register at the close of business on 26 November 2021.

CMC reiterates its prior guidance and expects FY 2022 net operating income to be between £250-280 million.

Lord Cruddas, Chief Executive Officer, commented:

“I’m very pleased to see the business is operating well above pre-pandemic levels across all our business lines. This is testament to the resilience and quality of our platform and offering.

Encouragingly for the future, we closed our first half with client money (“AUM”) in our leveraged business being maintained close to record highs. It was also encouraging to see active client numbers increase by 10% in our non-leveraged business in support of our diversification strategy. Our non-leveraged business continues to offer the greatest growth potential and now represents approximately 50% of our trading revenue in Australia and nearly 20% of Group net operating income.

In line with our aim to diversify and grow our non-leveraged earnings we announced the acquisition of the ANZ Share Investing clients that, when completed over a 12-18 month period, will boost our non-leveraged business with approximately 500,000 clients with total assets in excess of AUD$45bn. We are on a fast track to diversification, using our existing platform technology to win B2B and B2C non-leveraged business. This will be further boosted with the launch of our new UK investment platform planned in the early part of the next financial year, which will offer both B2C and B2B potential.

In line with this strategy, we believe it is right for us to evaluate the viability of separating the businesses in order to unlock the significant value within the current Group structure. The Board is expected to start this review before year end and complete it by June 2022. We will update on progress in due course.”