Worldline registers 9.3% Y/Y growth in H1 2023 revenue

Worldline SA (EPA:WLN), a global leader in payment services, today announced its results for the first six months of 2023.

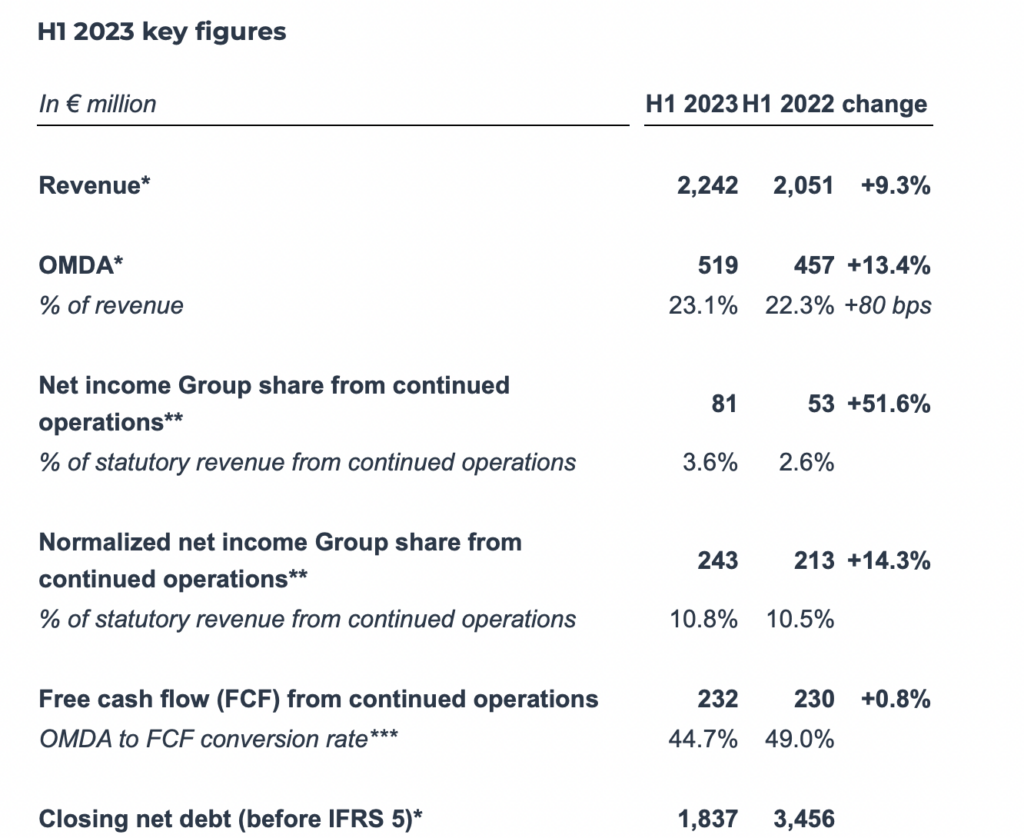

Worldline’s H1 2023 revenue reached € 2,242 million, representing +9.3% revenue organic growth (of which +9.4% in Q2). This achievement was reached thanks, in particular, to the continuous growth dynamic in Merchant Services reflecting the robustness of the business model. It reflects the benefit of the widespread and rapid shift towards digital payments as well as the Group’s strong positioning following the acquisition of Ingenico.

This strong execution also materialized in the Group’s Operating Margin before Depreciation and Amortization (OMDA) reaching € 519 million in H1 2023; representing 23.1% of revenue, an improvement by +80 basis points compared to H1 2022 at constant scope and exchange rates. This profitability improvement was led in particular by Merchant Services posting +100 basis points thanks to the acceleration of revenue growth fostering operating leverage; synergies from Ingenico; and effects of transversal productivity actions.

Net income Group share from continued operations reached € 81 million, an improvement of +5.6%. Normalized net income Group share from continued operations (excluding unusual and infrequent items, Group share, net of tax) reached € 243 million, up +14.3%.

Normalized basic EPS was € 0.86 in H1 2023 compared to € 0.76 in H1 2022. On a dilutive basis, it was up 10.5% to € 0.84.

Free cash flow from continued operations in H1 2023 was € 232 million, representing a 44.7% cash conversion of OMDA (free cash flow divided by OMDA), in line with the expected half-yearly pattern of 2023.

Group Net debt amounted to € 1,837 million at the end of June 2023, reflecting good free cash flow generated over the semester. It represents a Group leverage ratio at 1.6x on a LTM basis.

Worldline’s Q2 2023 revenue reached € 1,172 million, representing a +9.4% organic growth. This achievement was notably reached thanks to the solid growth in Merchant Services at +13.5% organically, fueled by payment volumes both instore and online in commercial acquiring activities. Financial Services was broadly stable, in line with anticipated full year trajectory. Mobility & e-Transactional Services benefited of a solid underlying growth but remained impacted, as already disclosed, by the re-insourcing of a secured mail telco operator contract end of Q2 22, leading to an overall flat performance in Q2 2023.