Wise upgrades its FY23 total income guidance

Wise plc (LON:WISE) today issued a trading update for the third quarter of fiscal year 2023, with the company revising upwards its forecast for FY23 income.

Wise reported 5.8 million customers having transacted with the company in Q3 FY23, an increase of 33% year-on-year and 6% quarter-on-quarter, comprising 5.5 million personal (+34% YoY) and 320,000 business customers (+26% YoY). This increase in active customers continues to be driven by strong new customer growth.

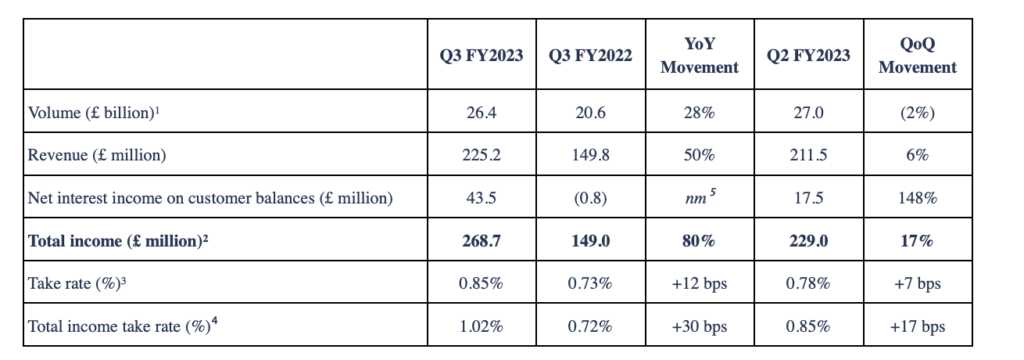

Total cross border volumes were £26.4 billion in Q3 FY23, 28% higher than in the same period last year. Personal customers moved £19.0 billion, a 26% increase compared with last year, reflecting the continued strong growth in active customers. Business volumes of £7.4 billion were 35% higher against the equivalent period a year earlier. On a constant currency basis, total volumes grew 23% in annual terms.

Compared with Q2 FY23, total volumes were 2% lower. Whilst VPC for business customers continued to increase quarter-on-quarter personal VPC was down 10%, primarily due to lower levels of activity in the high-volume cohorts of personal customers.

Revenue for Q3 FY23 was £225.2 million, up 50% from the corresponding quarter a year earlier and 6% quarter on quarter.

Total income, inclusive of net interest income, for Q3 FY23 was £268.7 million, an 80% increase on last year and the total income take rate increased 30 bps to 1.02%. Net interest income of £43.5 million was 148% higher than in Q2 FY23 due to higher rates on invested assets and continued growth in customer balances.

As a result of the continued growth in revenue this quarter, supported by the increase in net interest income, Wise is upgrading its FY23 total income guidance and now expects this to grow 68-72%, compared with 55-60% previously.

With a higher proportion of the net interest income to flow to EBITDA in the short-term, Wise expects its adjusted EBITDA margin for the second half of FY23 to be higher than the 22% in the first half of FY23. The medium-term guidance for total income and adjusted EBITDA margin remains unchanged.

Summary of forward looking guidance:

- Total income growth expected to be between 68-72% in FY23 and greater than 20% (CAGR) over the medium-term;

- Adjusted EBITDA margin for H2 FY23 expected to be higher than the 22% margin in H1 FY23; and

- Adjusted EBITDA margin at or above 20% over the medium-term.