Market betting on improved offer for Gain Capital / Forex.com

Retail FX brokerage operator GAIN Capital Holdings Inc took the interesting step yesterday of releasing its results for the month of April 2020, alongside its usual practice of disclosing monthly trading volumes. GAIN of course usually reports its financial figures – Revenues, EBITDA, Net Income et al – on a quarterly basis, as required of publicly traded companies in the US.

However GAIN’s board decided to take this unusual step in an apparent attempt to bolster the chances of its planned acquisition by larger rival INTL FCStone going ahead.

You see, GAIN seems to be somewhat the victim of its own near-term success. At the time when GAIN agreed to be acquired by FCStone it had just reported fairly poor results for 2019, seeing Revenues decrease by 35% and a net loss of $60.8 million (although things had turned around somewhat during the first two months of Q1-2020).

The agreement with FCStone was announced on February 27, just at the beginning of the market’s COVID-19 driven nosedive which ran through most of March. For most companies the month of March 2020 was trouble, but for Retail Forex brokers like GAIN’s Forex.com and City Index brands it was just what the doctor ordered. Heightened market volatility across nearly every instrument imaginable – equities, commodities, and of course FX – led to a huge spike in trading volumes for FX brokers, and thus robust Revenues and profitability.

When GAIN released its Q1 results on April 23, its shares (which had been trading in the $3.50 range before the FCStone deal came along) popped to above $6. That’s very significant, in that FCStone’s offer is for $6 in cash per GAIN share.

GAIN’s shares rose as dissent became evident on its board regarding the deal, and a number of large GAIN shareholders started to push GAIN CEO Glenn Stevens and the board to either abandon the acquisition, or at least renegotiate a higher price with FCStone.

The reason to question the acquisition versus going-it-alone became quite obvious when examining GAIN’s Q1 results. GAIN posted adjusted EBITDA of $114.4 million in Q1. Why sell a company for just $236 million, if it is pumping out cash flow of about half that amount in just 3 months?!

And if the market is always right (as day trading pioneer Jesse Livermore famously said), then the market certainly believes that the FCStone-GAIN deal will not just go ahead on its current terms, with GAIN’s share price continuing to climb and sitting at $6.48 currently, well above FCSTone’s $6 offer.

So back to GAIN Capital’s unusual release of April 2020 financial figures yesterday. What the board apparently attempted to do is show that the Q1 “windfall” was likely temporary, with March’s superb results being followed by a coming-back-down-to-earth in April.

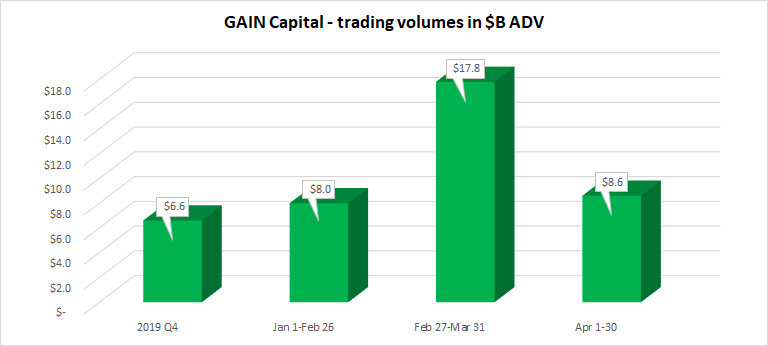

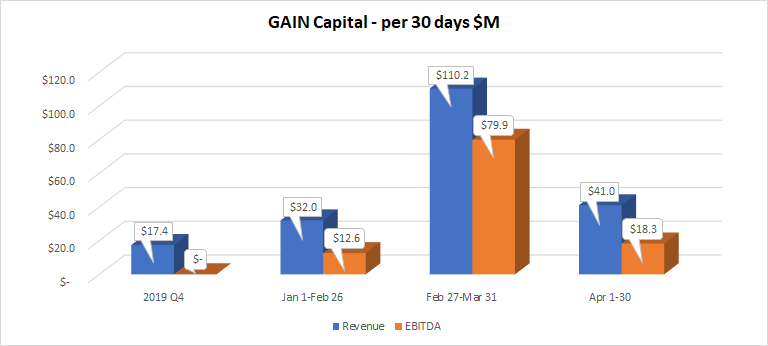

And indeed, GAIN did “hit it out of the park” in late February thru March, with the company reporting a per-month equivalent of $110.2 million in Revenue and nearly $80 million in EBITDA, on average daily trading volume of $17.8 billion – more than double the $8.0 billion ADV that Forex.com and City Index saw in the first two months of 2020, and nearly triple the $6.6 billion ADV in Q4-2019.

So again, if you can throw off $80 million in cash profit a month, why sell for $236 million?!

However GAIN’s board pointed out that despite continued market volatility throughout most of April, activity returned to a more normal (yet quite healthy) level leaving March’s pie-in-the-sky figures behind. GAIN Revenues slid back down to earth by more than 60% to $41 million in April, while EBITDA of $18.3 million – while certainly much better than the company was doing the past couple of years – was a far cry from $80 million monthly.

GAIN’s board pointed out that in addition to a $9 million breakup fee it will need to pay FCStone if it calls off the acquisition, a lot of risk still exists in going-it-alone. While the COVID-19 driven market crash (and subsequent rebound) did provide a big jump-start to GAIN’s near term results, like many companies in many industries the future in a very clouded one at GAIN.

GAIN did point out that the board’s continued support of the acquisition by FCStone at the $6-per-share price is not unanimous, with director Alex Goor voting against the proposal as-is.

So if indeed the market is always right, something is likely to give in the form of a better offer by FCStone, or perhaps even another suitor emerging at higher than $6 – that despite the board disclosing that it had run a lengthy and thorough auction process involving 108 potential bidders, before settling on the offer by FCStone.