Key Events to Follow Tomorrow: FOMC Minutes, RBNZ Decision

The following is a guest editorial courtesy of Carolane de Palmas, Markets Analyst at Retail FX and CFDs broker ActivTrades.

Tomorrow brings two major catalysts for the forex market. Traders will turn their attention to the FOMC minutes, which could shed light on the Fed’s path toward expected rate cuts in the coming months, before shifting focus to Chair Powell’s speech at Jackson Hole later this week. Before that, the spotlight in the Asia-Pacific region will be on the Reserve Bank of New Zealand’s policy decision, where markets are positioning for a potential rate hike. Together, these events could set the tone for currency markets by reshaping interest rate expectations on both sides of the Pacific, especially for the Forex pairs including the USD and the NZD.

The Reserve Bank of New-Zealand (RBNZ) Is Expected to Lower its Key Rate to 3%

The Reserve Bank of New Zealand (RBNZ) finds itself at a critical juncture. At its July meeting, the central bank decided to leave its key rate unchanged at 3.25%, stressing that elevated uncertainty made it prudent to wait for more economic data about inflation, growth, as well as the housing and job markets, before moving policy.

The RBNZ decided to wait before cutting interest rates so then they could evaluate whether domestic weakness was becoming entrenched, how inflation evolved, and how external developments — particularly the impact of U.S. tariffs and shifting global trade conditions — might affect New Zealand’s economic outlook.

But that period of patience now appears to be over.

Market participants are widely anticipating that the Monetary Policy Committee will cut the OCR by 25 basis points to 3% at its meeting on Wednesday, August 20, continuing the easing cycle after July’s pause. According to a Bloomberg survey, 22 of 23 economists expect a rate cut, which would bring borrowing costs to their lowest level in three years and align policy with what is broadly considered a neutral stance.

A cut would provide some relief to the domestic economy, where activity has been slowing under the weight of weak demand, softer business investment, and global trade pressures. Lower rates would help ease financial conditions, supporting households and exporters, but they also risk undermining the New Zealand dollar if markets interpret the move as the start of a deeper easing cycle. In contrast, a more cautious outlook from the RBNZ could lend the currency some resilience, especially given the parallel uncertainty surrounding U.S. monetary policy.

For traders, the key focus will not only be the rate decision itself but also the updated set of RBNZ projections. In May, forecasts pointed to the OCR declining to around 2.85% by early 2026, leaving the door open for further easing to as low as 2.75% if conditions warrant. Any signal that the central bank intends to accelerate or slow this trajectory could spark significant volatility in NZD pairs.

The global environment has become an increasingly important factor for the RBNZ, and recent trade tensions with the United States stand out as a key source of uncertainty. The central bank has already acknowledged that higher U.S. tariffs are likely to weigh on New Zealand’s economy by dampening both growth and inflation. With the United States being New Zealand’s second-largest export market, any reduction in demand for Kiwi goods could directly undermine export revenues, agricultural output, and manufacturing activity, while indirectly reshaping inflation expectations.

The stakes were raised after President Donald Trump announced a 15% tariff on New Zealand exports at the start of August, a measure that exceeded the 10% initially signalled. The policy was part of a broader U.S. decision to impose higher tariffs on countries running trade surpluses, and New Zealand was no exception.

In response, Agriculture, Forestry, Trade and Investment Minister Todd McClay announced a trip to Washington to engage in talks with U.S. officials, stressing that the visit would be an opportunity to outline the costs of the new tariff and gain a clearer sense of how U.S. trade policy may evolve in the months ahead. McClay underscored the depth of the long-standing trade partnership between the two countries, noting that surpluses have shifted over time and that overall trade has generally been complementary.

Yet, despite these reassurances, the domestic economy is already feeling the strain. Manufacturing output contracted in both May and June, service-sector activity has now been in decline for 17 consecutive months, and unemployment has risen to 5.2%, its highest level in five years. Housing markets, once a powerful driver of consumer wealth, have stagnated since the retreat from their pandemic surge. These developments highlight the fragility of domestic demand and reinforce why external shocks like U.S. tariffs carry such weight in shaping the RBNZ’s outlook.

Inflation, meanwhile, remains caught in a delicate balance. It quickened to 2.7% in the second quarter, after reaching 2.5% in the March quarter. While inflation is edging toward the top of the RBNZ’s 1 to 3% target band, policymakers continue to expect that inflation will gradually cool, returning to around 2% by early 2026. The risk, however, is that weaker trade flows and reduced export competitiveness accelerate this disinflationary trend, justifying a more accommodative stance in monetary policy sooner rather than later.

Dollar Traders Eye Fed Minutes for Clues on Policy Shift

The release of the Federal Reserve’s minutes from its most recent meeting will be a crucial moment for traders this week, as markets look for confirmation that U.S. rate cuts are back on the table. Investors are increasingly convinced that the central bank will lower borrowing costs in September, with U.S. money markets currently pricing in a 93.5% probability of a 25 basis-point reduction, according to LSEG data. The minutes could either reinforce this conviction or inject doubt, setting the stage for heightened volatility across dollar pairs.

The July meeting itself was historic in its own right. For the first time since 1993, multiple Fed governors broke ranks with the majority decision. Michelle Bowman and Christopher Waller openly favored a quarter-point cut, underscoring the growing internal debate about whether the Fed should move more aggressively to support a slowing economy.

Recent data has tilted the balance toward easing. Softer-than-expected labor market figures and inflation readings that showed little evidence of tariff-driven price pressures have eased concerns about cutting rates too soon. For markets, this reinforces the expectation that a September move is coming, with some policymakers and officials even pushing for a bolder step. Treasury Secretary Scott Bessent has floated the idea of a 50 basis-point cut, while President Trump has repeatedly pressured Powell for failing to lower rates earlier this year, turning monetary policy into a politically charged arena.

If the minutes show broad support for near-term easing, the dollar could come under renewed pressure as rate differentials shift against it, particularly versus higher-yielding currencies. On the other hand, if the document signals hesitancy among FOMC members or resistance to larger cuts, the market may scale back its expectations, giving the dollar some short-term support. Either way, the minutes are set to be a pivotal driver of FX market sentiment ahead of Powell’s speech at Jackson Hole later in the week.

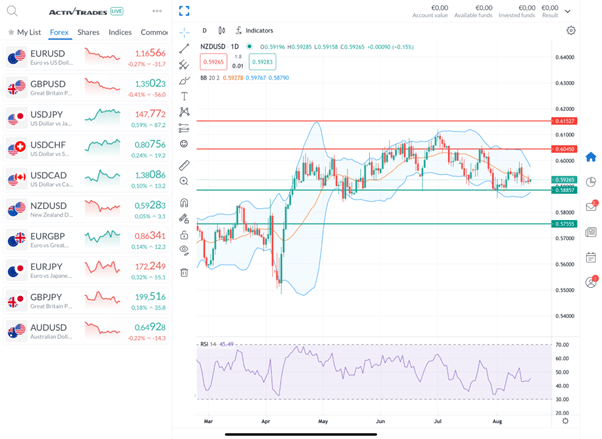

Technical Outlook of the NZD/USD Pair

Daily NZD/USD Chart from the ActivTrades’ Online Trading Platform

Sources: RBNZ, The Wall Street Journal, ActivTrades

The information provided does not constitute investment research. The material has not been prepared in accordance with the legal requirements designed to promote the independence of investment research and as such is to be considered to be a marketing communication.

All information has been prepared by ActivTrades (“AT”). The information does not contain a record of AT’s prices, or an offer of or solicitation for a transaction in any financial instrument. No representation or warranty is given as to the accuracy or completeness of this information.

Any material provided does not have regard to the specific investment objective and financial situation of any person who may receive it. Past performance is not a reliable indicator of future performance. AT provides an execution-only service. Consequently, any person acting on the information provided does so at their own risk. Forecasts are not guarantees. Rates may change. Political risk is unpredictable. Central bank actions may vary. Platforms’ tools do not guarantee success.