Is the 2026 KOSPI Sell-Off a Classic ‘Buy the Dip’ Moment?

The following is a guest editorial courtesy of Carolane de Palmas, Markets Analyst at Retail FX and CFDs broker ActivTrades.

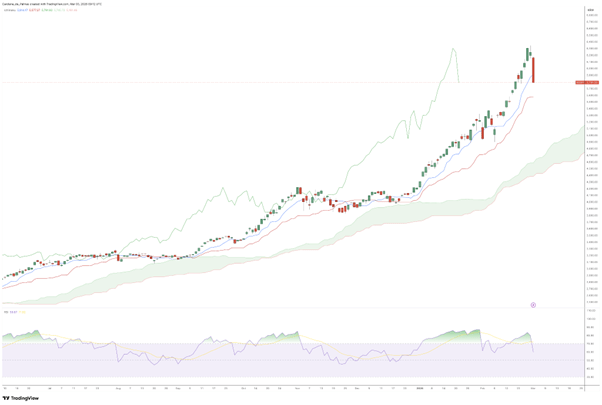

South Korea’s benchmark index suffered its worst single-day decline since August 2024 on Tuesday, shedding more than 7% amid mounting tensions in the Middle East. Yet this sharp retreat follows an extraordinary run: the KOSPI crossed the 5,000 threshold in late January before surging past 6,000 on February 25—a milestone reached less than a month later. Even after today’s tumble, the index remains up over 37% year-to-date, having already delivered a cumulative gain of more than 112% over the past two years.

Daily Chart of the KOSPI index – Source: TradingView

Some investors wonder if this is the beginning of a deeper correction or if they should “buy the dip”. Well, most analysts believe that there is still room for the South Korean index to grow. Below, we examine the key pillars that could support continued appreciation in 2026—alongside the risks that deserve careful consideration if you plan on investing in South Korea.

1. Exceptional Earnings Growth & Attractive Valuations

Perhaps the most compelling argument for South Korean equities lies in their fundamental value. Aggregate earnings across the Seoul market expanded by approximately 36% in 2025—and analysts at Goldman Sachs project that growth could accelerate dramatically, forecasting a further increase of up to 120% in 2026. That level of earnings momentum is, in the bank’s own words, “remarkably strong.”

Valuations remain undemanding in spite of recent index gains. The KOSPI currently trades at a 12-month forward price-to-earnings multiple of around 8.7x, falling to just around 7.8x on a 24-month forward basis. By global standards, these multiples are low, particularly for a market exhibiting this degree of earnings dynamism. In other words, even after a historic rally, South Korean equities may still represent a significant discount relative to the growth on offer.

While KOSPI earnings look strong, the Middle East conflict is the ultimate wild card. According to Goldman Sachs, there is a direct correlation between energy costs and profitability. The bank estimates that a 20% increase in oil prices could lead to a 2% decline in regional earnings. The silver lining? These spikes typically trigger knee-jerk sell-offs that dissipate as the market stabilizes.

2. A Structural Shift in Corporate Governance

For years, South Korean equities have traded at a persistent discount to regional and global peers: a phenomenon widely referred to as the “Korea Discount.” The primary drivers have been opaque ownership structures within family-controlled conglomerates, known as chaebols, and policies that historically favoured controlling shareholders over minority investors.

That structural dynamic is now changing. Under President Lee Jae Myung’s administration, a sweeping corporate reform agenda—branded the “Value-Up” initiative—has gained significant legislative traction. The National Assembly recently enacted a revision to the Commercial Act requiring companies to cancel newly acquired treasury shares within one year. This measure closes a long-standing loophole that allowed controlling families to use buybacks as a tool for consolidating influence rather than returning capital to shareholders.

Further reforms have followed. Parliament passed legislation mandating that company directors legally consider the interests of all shareholders, not merely the conglomerate’s ruling family. Cumulative voting rules now allow minority investors to concentrate their influence in board elections, and auditors must be elected through a separate process, insulating them from undue management control.

Additional measures include proposed tax incentives for companies that maintain dividend payout ratios above 35%, and a reduction in capital gains thresholds targeting major shareholders. These reforms are designed to narrow the gap between Korean equities and their international counterparts, making the market structurally more rewarding for outside investors. While politically sensitive inheritance tax reform—where rates can reach as high as 60%—has yet to be addressed, the direction of policy travel is meaningfully pro-investor.

3. Semiconductor Dominance and the AI Supply Chain

South Korea occupies a uniquely powerful position in the global technology landscape. Its two semiconductor champions, Samsung Electronics and SK Hynix, together control over 80% of the world market for high-bandwidth memory (HBM)—the critical chip component that powers artificial intelligence servers worldwide. The AI infrastructure buildout is still in its early stages, and demand for HBM shows no sign of slowing.

The financial impact has been deep. Samsung and SK Hynix together contributed approximately 40% of the KOSPI’s total gains last year, underscoring the degree to which Korea’s equity market has become a leveraged play on the global AI boom. Technology and industrial sectors combined represented close to 70% of the MSCI Korea Index’s total return in 2025, reflecting both the scale of the AI-linked rally and the breadth of Korea’s advanced manufacturing ecosystem.

Beyond semiconductors, South Korea maintains dominant positions across a range of next-generation industries, including advanced display technology, electric vehicle battery manufacturing, and components for the emerging new energy supply chain. This diversified technological specialisation provides multiple avenues for export-driven growth as the global economy transitions toward cleaner energy and greater digitisation.

4. World-Class Human Capital and Infrastructure

South Korea’s economic competitiveness is underpinned by structural advantages that extend well beyond any single industry cycle. The country consistently ranks among the world leaders in research and development spending as a share of GDP, and its education system produces an exceptionally well-trained pool of engineers, scientists and technology professionals.

Physical and digital infrastructure are similarly advanced. Broadband penetration, logistics networks, and port capacity all place South Korea at the frontier of connected, export-oriented economies. These assets, built over decades of investment, are not easily replicated and serve as a durable foundation for sustained industrial competitiveness, regardless of near-term market volatility.

Conclusion: Opportunity and Risk in Equal Measure

Tuesday’s sell-off is painful, but the structural story underpinning South Korean equities has not changed in a single session. The convergence of robust earnings growth, deeply discounted valuations, meaningful governance reform, and an unrivalled position in AI-enabling hardware represents a genuinely compelling investment case.

That said, risks cannot be dismissed. The market’s very strengths introduce concentration risk: with nearly 70% of recent index returns driven by the technology and industrial sectors, and the two semiconductor giants alone responsible for roughly 40% of gains, any disruption to global AI spending, export restrictions, or chip pricing dynamics could prove disproportionately damaging.

Geopolitical pressures—from the ongoing situation in the Middle East, which is already pushing energy costs higher, to the ever-present risk calculus surrounding the Korean peninsula—add an additional layer of uncertainty. Goldman Sachs analysts note that while geopolitical spikes tend to be temporary in their market impact, the current environment coincides with a period when Asian equities are already vulnerable to a technical correction after outsized gains.

The Korea Discount may be narrowing, but it has not disappeared. Inheritance tax structures and chaebol influence remain powerful forces working against a full valuation re-rating. And while the Value-Up initiative represents genuine progress, its long-term impact will depend on consistent implementation and political durability.

For investors with the appetite for volatility and a multi-year horizon, a dip—in a market with this earnings trajectory and these structural tailwinds—may well prove to be an interesting entry point. Still, it might be wise to hold off until we see how geopolitical tensions in the Middle East actually hit global growth and/or central bank policies.

Sources: Reuters, The Financial Times, MorningStar, Aberdeen, Goldman Sachs, Morgan Stanley, Credit Agricole, National Assembly of the Republic of Korea, Korean Ministry of Finance, MSCI Korea Index Data.

The information provided does not constitute investment research. The material has not been prepared in accordance with the legal requirements designed to promote the independence of investment research and as such is to be considered to be a marketing communication.

All information has been prepared by ActivTrades (“AT”). The information does not contain a record of AT’s prices, or an offer of or solicitation for a transaction in any financial instrument. No representation or warranty is given as to the accuracy or completeness of this information.

Any material provided does not have regard to the specific investment objective and financial situation of any person who may receive it. Past performance is not a reliable indicator of future performance. AT provides an execution-only service. Consequently, any person acting on the information provided does so at their own risk. Forecasts are not guarantees. Rates may change. Political risk is unpredictable. Central bank actions may vary. Platforms’ tools do not guarantee success.