European Banking Crisis: Who Stands to Lose or Gain?

The following is a guest editorial courtesy of Andrew Lane, CEO of sentiment-based technology company Acuity Trading.

On September 10, 2008, Lehman Brothers CFO Ian Lowitt said at the bank’s quarterly earnings call, “I think our capital position at the moment is strong.” Lehman Brothers had just reported its first loss-making quarter in 14 years and a restructuring of top management. The bank had spent the better part of the year assuring investors that it could weather any impending storms. Just five days later, Lehman Brothers filed for bankruptcy, amid a global financial crisis.

Today, some analysts fear a similar story unravelling in Europe. Two of the continent’s biggest banks, Credit Suisse and Deutsche Bank, have triggered concerns amid a possible recession. Credit Suisse and Deutsche Bank have both seen their share price tumble, by 56.28% and 39.52% year to date, respectively. The Credit Default Swap (CDS) spread, the price of insurance against a security default, for Credit Suisse hit a record high on October 3, before easing the next day after the bank announced a debt buy-back programme.

What’s Happening at These Banking Majors?

Credit Suisse has had a scandal-ridden few years. These damaging, and ultimately costly, scandals include the high-profile failure of investments in Greensill Capital and Archegos Capital, as well as a guilty verdict for Credit Suisse’s inability to prevent money laundering by Bulgarian drug traffickers. Credit Suisse CEO Ulrich Korner has insisted in a leaked internal memo that despite its legal troubles and whispers of a collapse, employees should not be confusing day-to-day stock performance with the bank’s strong capital base and liquidity position.

Deutsche Bank has been similarly reiterating the strength of its position. The German bank has recently completed a long-attempted restructuring effort, delivering a cost-cutting program that analysts expect to be successful.

The crux of the wider market fear is that, like Lehman in the noughties, the collapse or the constant shrinking of institutions like Credit Suisse and Deutsche Bank may lead to a contagion effect, resulting in more high-value failures. On the other hand, these banks are more than four times the size of Lehman at its failure.

Who Could Lose in a European Banking Crisis?

A banking crisis is when multiple financial intermediaries in an economy experience serious solvency or liquidity problems at the same time. When depository institutions fail, the first line of panic is formed by the depositors. A panicked depositor base, especially with recessionary fears brewing, would prefer to have their deposits in hand rather than at a bank facing the risk of failing. This causes a worsening of the crisis. Banks that are the largest in the economy they serve, such as Nordea in Finland, represent a higher risk of default once such a crisis begins to unfold.

Dutch financial services firm, ING, is among the European banks that are most sensitive to interest rates. There has been significant short interest in ING of late, after the firm said that profitability in its lending business had declined due to tighter net interest income. Banco Santander’s margins are already under pressure due to higher taxes imposed on banks by the Spanish government, which aims to generate around $7.02 billion over the next couple of years.

Germany’s 10-year yield, which is considered the benchmark for the euro bloc, has risen from below the closely watched 1% level on August 1 to more than 2.4% as of October 12, hitting its highest level since August 2011. Britain’s 10-year Gilt also reached near a 14-year high on that day. Despite high inflation, bond yields in Europe could fall, with investors expecting the ECB to refrain from aggressive monetary tightening in the face of a recession.

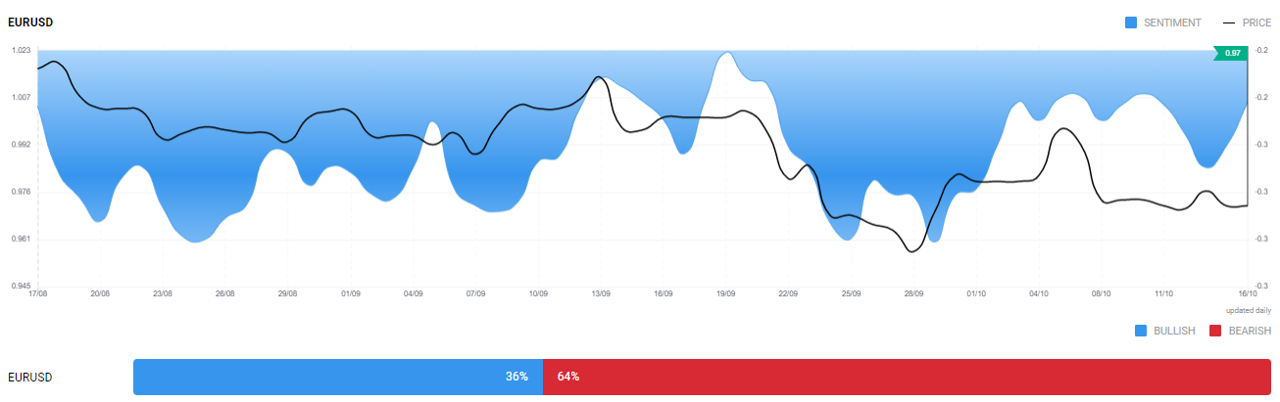

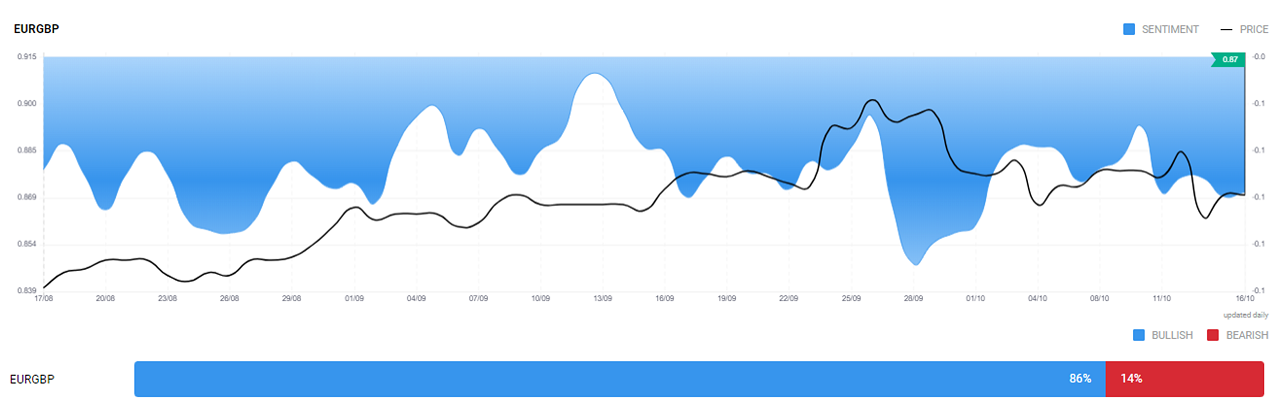

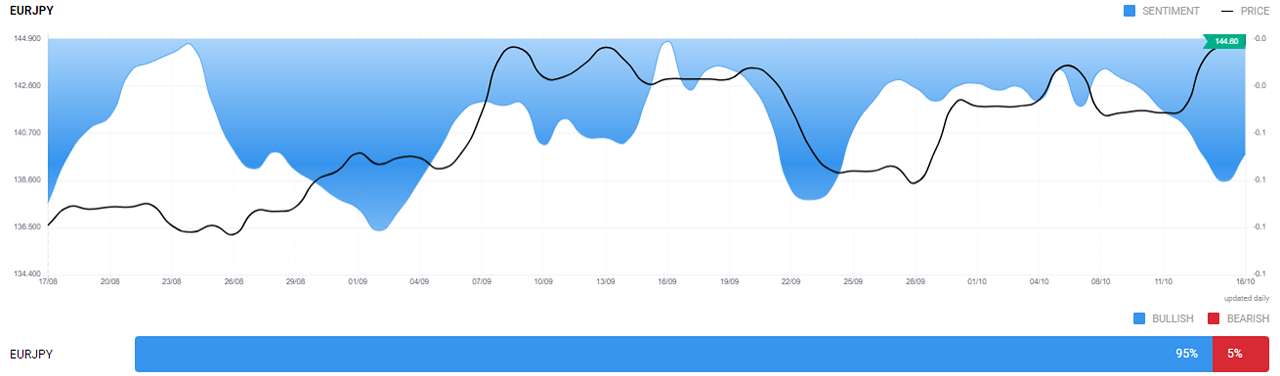

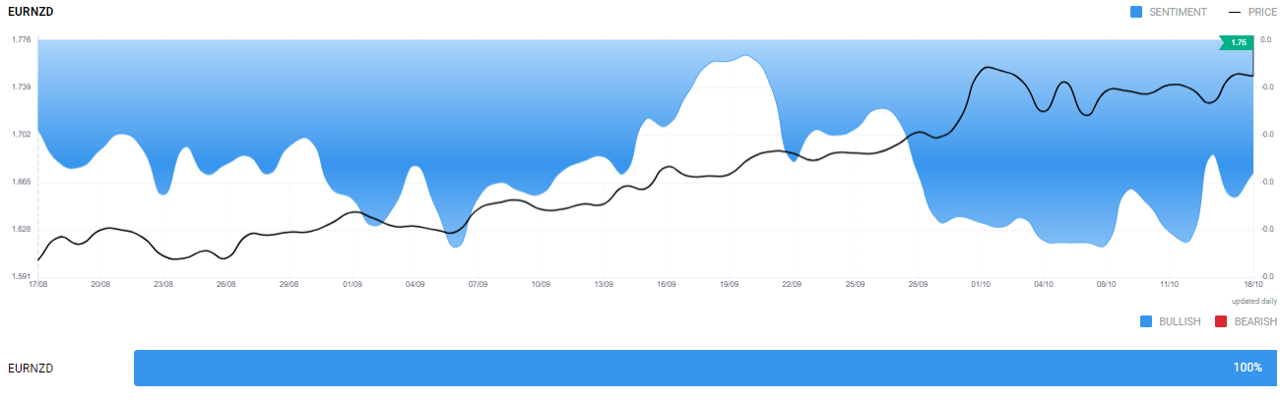

The euro will also probably not shine amid a potential banking crisis. The ECB is already unable to out-hawk the US Federal Reserve. The difference could widen, shaving off the euro’s power in currency carry trades. The Acuity Trading Widget reflects a more favourable sentiment for the US dollar versus the euro.

However, this could well be due to the massive Fed rate hikes, rather than concerns around the euro. In fact, the sentiment for the euro is very favourable when compared to other major currencies like the British pound, the Japanese yen or even the New Zealand dollar.

A banking crisis may also lead to a drying up of credit. Banks, wary of defaults, may begin to reduce their lending, adversely impacting various sectors. There are some sectors that investors may think of shorting as the European economy braces for more trouble ahead.

Who Could Gain from a European Banking Crisis?

The valuations of European stocks have fallen below their long-term average. Shares of several companies have hit 52-week lows. However, European stock valuations are still higher than the lows hit during the 2008 crisis. The unfolding of a banking crisis could change that. European stocks becoming much cheaper than their US peers would attract investors from across the pound.

Investors who shop amongst the debris have the advantage of finding stocks at dirt cheap prices. In 2008, Warren Buffet declared he was buying American stocks during the then ongoing crisis. The Oracle of Omaha invested in Goldman Sachs, GE, Swiss Re and Dow Chemical, and benefited from the recovery. In 2009, hedge fund manager John Paulson converted his bets against the US housing markets to bets in favour of the housing market, posting profits.

One needs to choose the securities very carefully. Investors can consider following the money and pick out companies and banks where the big money deals are taking place.

The downturn in the European stock market also creates hedging opportunities, with a significant reduction in the cost of portfolio protection. For instance, Germany’s DAX 50 has become particularly appealing, after its selloff due to its high exposure to energy-intensive sectors, like industrials, autos and chemicals.

Another potential beneficiary of a European Banking Crisis is the equity markets in other developed countries and emerging economies. The US and China stock markets may see an inflow of capital.

Investors may also add more safe-haven assets in their portfolios, lending upside to gold, silver, the US dollar and the Japanese yen. Moreover, consumer staples may also see some upside.

Conclusion

While there may be bouts of volatility in the equity markets over the next couple of months, a banking crisis in Europe is far from being a certainty. The region does face macroeconomic headwinds from an economic slowdown and soaring inflation. However, the European Banking System is regularly stress tested by regulatory authorities. Regulatory changes have made the chance of a Lehman-styled contagion very low in the case of Credit Suisse and Deutsche Bank. However, examining black swan events is crucial to forming an investment ideology.

In a banking crisis, winning often requires reading market cues from investment in the recovery, or parking your funds in relatively sheltered assets until feasible investment opportunities arise.